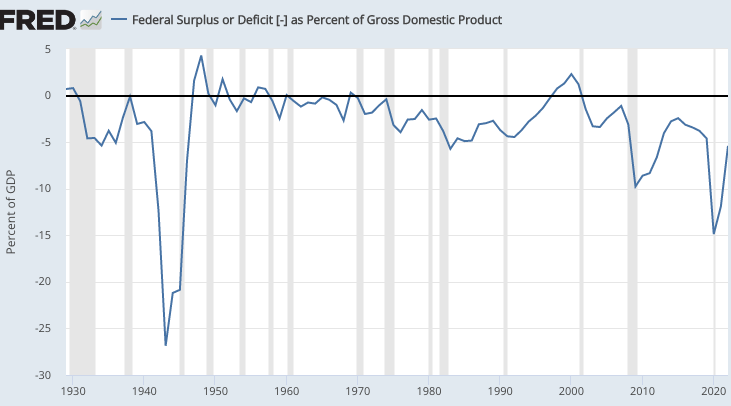

One of the worst depressions in American history began in mid-1937. At the time, Keynesian ideas were becoming increasingly prominent and many Keynesians blamed fiscal austerity. In fact, there wasn’t all that much fiscal austerity in 1937, certainly not enough to cause a major depression:

Between 2020 and 2022 we had roughly twice as much “austerity” as in 1937, at least in terms of the reduction in the budget deficit. And yet not only did we not have a major depression, we saw some of the strongest job growth in American history. Yes, we began 2022 with employment still a bit below normal, but that was even more true in 1937. And yes, the austerity of 2022 mostly reflected the decision to end COVID relief programs, but much of the austerity of 1937 was the decision to not repeat the big 1936 “bonus” payments to WWI veterans.

I’m confident that observers can spot a few more differences, but do they actually explain such a dramatic difference in outcome? Do they explain the difference between major depression and extraordinary job growth? And why didn’t the sharp fiscal tightening after WWII lead to the major depression predicted by Keynesian economists at the time? Why didn’t the big 1968 tax increase reduce inflation, as predicted by Keynesian economists? Why didn’t the 2013 austerity produce a recession, as predicted by Keynesian economists?

The answer to all of these questions is quite simple: it’s monetary policy that drives aggregate spending, not fiscal policy. Tight money caused the 1937 depression. It’s time to give up on the theory that fiscal policy drives aggregate demand. The Fed takes fiscal policy into account when it makes its decisions. It tries (not always successfully) to offset the effects.

The same concept applies to banking problems. It is very possible that we’ll have a recession in late 2023 (recessions are almost impossible to forecast.) But if we do, it won’t be caused by banking turmoil. If the Fed thought credit problems were likely to lead to a recession, they would not be raising interest rates this week. If there is a major recession it will be because the Fed raised rates too much—it misjudged the situation. In contrast, a very small recession might in some sense be intentional—the Fed’s way of reducing inflation.

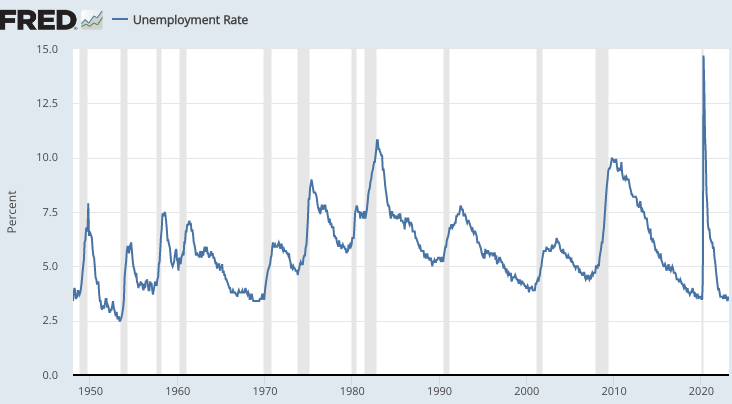

P.S. Here’s the unemployment rate. Notice that recessions (grey vertical bars) are easy to spot. Do you see a recession in 2022? Neither do I.

READER COMMENTS

Jon Murphy

May 3 2023 at 5:22pm

I was about to say that, surprisingly, I do. But then I realized the gray bar I was looking at was actually the right border of the graph…

John Hall

May 3 2023 at 6:19pm

And here I am not being able to see any grey bars…

Garrett

May 3 2023 at 10:20pm

I listened to Powell’s speech today and it seems like the market thinks the Fed will pause in June and probably cut in July. I look at CPI and the trend has been consistent since last June at a higher rate than pre-covid. Not sure how the Fed expects to get 2% inflation without hiking more.

Thomas Hutcheson

May 3 2023 at 11:55pm

TIPS thinks the Fed has over done it will not keep inflation up to target over the long run.

Dale Doback

May 4 2023 at 2:00pm

Where are you getting that data from? 5 and 10 year tips breakevens are still over 2%.

Brent Buckner

May 5 2023 at 10:33am

TIPS breakevens involve headline CPI; the stated Fed target is headline PCE.

“Between the two headline indexes, the CPI tends to show more inflation than the PCE. From January 1995 to May 2013, the average rate of inflation was 2.4 percent when measured by headline CPI and 2.0 percent when measured by headline PCE.” — https://www.bls.gov/osmr/research-papers/2017/st170010.htm

(There are also liquidity effects that mean TIPS breakevens do not make for a simple translation even to market expectations of CPI.)

Thomas L Hutcheson

May 4 2023 at 7:45am

Eventually we are going to learn that macroeconomic outcomes (not jut inflation, Milton :)) are monetary instrument setting outcomes (allowing for the fact that the setting may be inconsistent with the policy.

Spencer

May 4 2023 at 1:45pm

If you wanted to wreck the economy, you’d do exactly what Powell is doing.

Waller, Williams, and Logan seem to agree. They “believe the Fed can keep unloading bonds even when officials cut interest rates at some future date.”

The correct response to stagflation is the 1966 Interest Rate Adjustment Act. “while the aggregate of time and demand deposits continued to increase after July, the proportion of time to demand deposits diminished. Whereas time deposits were 105 percent of demand deposits in July, by the end of the year, the proportion had fallen to 98 percent. These were all desirable developments.

”M1 peaked @137.2 on 1/1/1966 and didn’t exceed that # until 9/1/1967.

Deposit rates of banks, Reg. Q ceilings, decreased from a high range of 5 1/2 to a low range of 4 % (albeit not enough). A .75% interest rate differential was given to the nonbanks. And during this period, the unemployment rate and inflation rates fell. And real interest rates rose. And there was no recession with an inverted yield curve.

Spencer

May 4 2023 at 1:51pm

“Pushing on a string” only applied prior to the nominal legal adherence to the fallacious “Real Bills Doctrine” which was terminated in 1932 – due to a paucity of eligible (hopelessly impaired), commercial and agricultural paper for the 12 District Reserve bank’s discounting purposes.

Gov’ts weren’t made eligible until the 1933 Glass-Steagall Act, or U.S. Banking Act of 1933, with the (with further liberalization of the eligible collateral accepted provided in the Banking Act of 1935 – “secured to the satisfaction of the Federal Reserve Bank”).

Between 1929 (@ $183.2b) & 1939 (@ $189.9b), there was no overall expansion of net debt (within the Great Depression). Then during 1940-1945 total real debt expanded by approximately $193.5b (therein cumulative net debt doubled in 5 years).

In 1932, as the FDIC highlights: “the interest rate on U.S. Treasury bills became negative because investors were willing to take a loss if they knew that their money was safe.” Especially with its taxing authority, the Federal gov’t is now the largest creditworthy borrower.

Spencer

May 4 2023 at 5:01pm

You don’t get a recession unless the 10-month rate-0f-change in money flows, the volume and velocity of means-of-payment money, the proxy for R-gDp, turns negative.

I got the 10mo roc in RRs from The Bank Credit Analyst, from their debit/loan ratio.

As Dr. Richard G. Anderson (Ph.D. Economics, MIT), Emeritus, FRB-STL (world’s leading guru on bank reserves), stated: Sent: Thu 11/16/06 9:55 AM:

“Today, with bank reserves largely driven by bank payments (debits), your views on bank debits and legal reserves sound right!”

In 1931 a commission was established on Member Bank Reserve Requirements. The commission completed their recommendations after a 7-year inquiry on Feb. 5, 1938.

The study was entitled “Member Bank Reserve Requirements — Analysis of Committee Proposal”

its 2nd proposal: “Requirements against debits to deposits”

After a 45 year hiatus, this research paper was “declassified” on March 23, 1983. By the time this paper was “declassified”, Nobel Laureate Dr. Milton Friedman had declared RRs to be a “tax” [sic].

Spencer

May 5 2023 at 10:34am

Reuters: “These officials also noted the Fed at some point could even lower short-term interest rates as it continues to draw down the roughly $8.5 trillion balance sheet, and that such a move would not be at odds with wider monetary policy.”The FED should cut interest rates NOW – and continue with QT. The 1966 Interest Rate Adjustment Act is prima facie evidence.

The GOSPEL

https://fraser.stlouisfed.org/files/docs/meltzer/bogsub020538.pdf

Tiberius

May 16 2023 at 4:04pm

I’m not going to argue that paleo-Keynesianism is a valid policy stance in 2023, but saying we had “austerity” between 2020 and 2022 is highly disingenuous. The policymakers in Washington certainly wouldn’t have called it that. Also, why did you fail to mention the record-setting “austerity” of the mid-1940s, when the U.S. transitioned to a war economy and federal spending as a percent of GDP reached its highest levels ever? You are obviously being facetious to make a confusing and somewhat contradictory point.

This is tantamount to an admission that fiscal policy is not irrelevant, even as you downplay its effects. Do you believe the Fed could have managed the unprecedented plunge in aggregate demand caused by COVID on their own, without increased fiscal spending, simply through monetary policy? If we ascribe any value to the unemployment rate, it is quite clear that the combined monetary + fiscal policy response to the COVID shock was more effective than the response to the 2008 financial crisis. I think a lot of well-respected people would agree that a key distinction was the more aggressive fiscal approach to the COVID shutdowns, but I suppose if your agenda is to always criticize and downplay the effects of government spending, you might protest this conclusion. And since monetary policy changes are far more flexible and adaptable than fiscal policy changes, and can always be implemented more quickly, it’s very easy to just point to the Fed’s response to fiscal policy and claim that it was the *real* underlying force at play, and that the same results could have been achieved with no fiscal response at all. But this is an unfalsifiable hypothesis.

Federal government outlays as a percent of GDP were <10% pre-WWII, and have since hovered around 15-20%, until COVID when they spiked to 30%. Total bank assets, on the other hand, have been consistently above 50% of GDP since the 1970s (FRED doesn’t have data for earlier), and in the 21st century have trended toward 75%. Fed actions by nature thus exert a much broader impact on the economy. And if you use this fact to argue against future fiscal policy responses, the self-fulfilling nature of this argument grows even stronger. The question of whether or not fiscal policy was warranted in any given situation should not be judged only by its relative impact on the economy compared to monetary policy. Anyone who received a stimulus check or a PPP loan can attest to the fact that they weren’t irrelevant.

Comments are closed.