A Century of Irish Economic Independence: "The Celtic Tiger" and Beyond

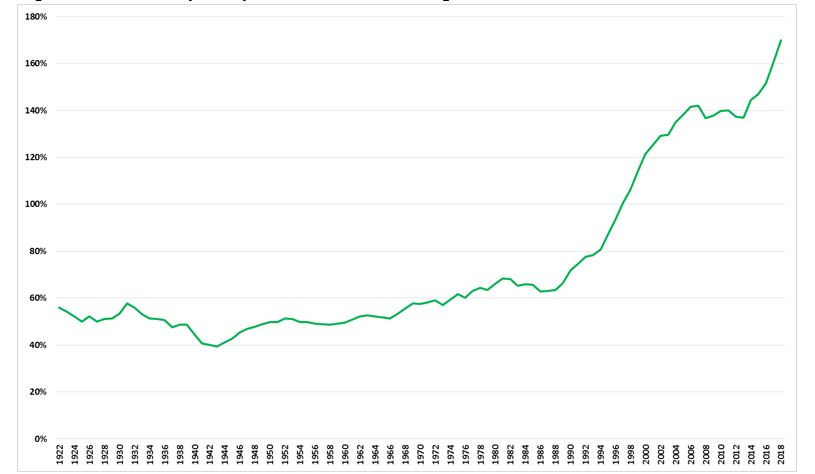

The first decades of Irish independence would have been an economic disappointment to those who birthed the nation in 1922. Then, Irish per capita GDP was 56% that of the United Kingdom: by 1988 it had risen to just 64% and The Economist carried an article on Ireland titled ‘The poorest of the rich’.

Figure 1: Irish GDP per capita as % of United Kingdom’s

Source: Maddison Project

In 1997 Irish per capita GDP exceeded that of the United Kingdom for the first time (Figure 1) and The Economist now hailed the ‘Celtic Tiger’. Why did Ireland, so poor, suddenly become so rich?

The poorest of the rich

Ireland’s economy was badly mismanaged in the 1970s. Governments ran ever larger deficits and as a share of GDP Irish government debt rose from 40% in 1971 to 95% in 1991. This brought no economic benefit: unemployment rose from 6.6% in 1971 to 17.6% in 1987. The economist Dermot McAleese wrote that “high taxes, low confidence, high labour costs, excessive regulation and anti-competitive practices” plagued the Irish economy in the 1980s. Ireland’s accession to the European Economic Community in 1973 brought no respite from these economic woes.

The Celtic Tiger

By the end of the 1980s it was obvious that this was unsustainable. The government — with wide support — slashed spending and made credible commitments not to run deficits or inflate the currency. It deregulated and lowered tax rates. The 2002 Index of Economic Freedom ranked Ireland the world’s 4th freest economy.

Ireland’s corporate tax rate – 12.5% – is famously low, but there was more to Celtic Tiger fiscal policy than that. As economist Sean Dorgan argues, since 1987:

…personal tax rates have been reduced progressively from a base rate of 35 percent to 20 percent and from a top rate of 58 percent to 42 percent. Tax bands (brackets) have also been broadened so that the higher rate now applies to higher income levels than before. The power of low rates was also shown when the 40 percent capital gains tax rate was halved in 1999 to 20 percent and revenue increased by 50 percent in one year and by 270 percent over three years.

McAleese argues that controlling government spending was crucial:

The espousal of fiscal rectitude and new consensus economic policies was not in fact new. What was new was the decision to attack the debt by controlling public spending, rather than by increasing taxes. For a small, open economy, curbing public spending proved a far more productive way forward. It created room for tax cuts while simultaneously lowering the debt ratio. Another ploy was the introduction of a tax amnesty. Following on the high tax policy of the 1980s and the reorientation in fiscal policy, it proved hugely successful in terms of revenue generation. Domestic interest rates fell steeply as investor confidence grew, thus starting off that rare occurrence in modern economics, an expansionary fiscal contraction. Fears that strong fiscal contraction would prove deflationary were confounded, though precisely why this was so remains the subject of controversy.

The results were striking. Ireland’s economy grew at an average annual rate of 9.4 percent between 1995 and 2000. Real GDP growth outpaced that in the United Kingdom in every year from 1989 to 2003 and of the United States in every year after 1993. While Ireland’s GDP grew by 229 percent between 1987 and 2007, the figure was 161% for the United States and 152% for the United Kingdom. Government debt fell from 95% of GDP in 1991 to 25% in 2007 and unemployment fell from 17.6% in 1987 to 3.4% in 2001.

The bust

In 2008 this came to a shuddering halt. Growth collapsed and government debt and unemployment rocketed.

Some blamed Ireland’s low tax and light regulation policies. The reality was rather different, as economist Patrick Honohan explained:

Until about 2000, the growth had been on a secure export-led basis, underpinned by wage restraint. However, from about 2000 the character of the growth changed: a property price and construction bubble took hold…Among the triggers for the property bubble was the sharp fall in interest rates following euro membership.

In short, there had been a good Celtic Tiger, based on sound money, low taxes, and light regulation, which had been replaced by a bad Celtic Tiger based on cheap credit following Ireland’s entry into the euro. True, there was much to condemn in the excesses of the boom’s later stages, but the fiscal and regulatory policies which had spurred a decade of solid growth were not among them.

The primacy of domestic policy (again)

In the century since ‘Irexit’ from the United Kingdom, Ireland’s economy has fared badly and fared well. Whether it has fared badly or well has not primarily, or even largely, been determined by its membership of the United Kingdom or even the European Union. It has been determined primarily, instead, by domestic policy decisions. So it will be with other more recent ‘exits’.

John Phelan is an Economist at Center of the American Experiment.