Why Default on U.S. Treasuries is Likely

By Jeffrey Rogers Hummel

“Buried within the October 3, 2008 bailout bill was a provision permitting the Fed to pay interest on bank reserves. Within days, the Fed implemented this new power, essentially converting bank reserves into more government debt. Now, any seigniorage that government gains from creating bank reserves will completely vanish or be greatly reduced.”

To understand why, we must look at U.S. fiscal history. Economists refer to the revenue that government or its central bank generates through monetary expansion as seigniorage. Outside of America’s two hyperinflations (during the Revolution and under the Confederacy during the Civil War), seigniorage in this country peaked during World War II, when it covered nearly a quarter of the war’s cost and amounted to about 12 percent of Gross Domestic Product (GDP). By the Great Inflation of the 1970s, seigniorage was below two percent of federal expenditures or less than half a percent of GDP.1 This was partly a result of globalization, in which international competition disciplines central banks. And it also was the result of sophisticated financial systems, with fractional reserve banking, in which most of the money that people actually hold is created privately, by banks and other financial institutions, rather than by government. Consider how little of your own cash balances are in the form of

government-issued Federal Reserve notes and Treasury coin, rather than in

the form of privately created bank deposits and money market funds.

Privately created money, even when its quantity expands, provides no

income to government. Consequently, seigniorage has become a trivial source of revenue, not just in the United States, but also throughout the developed world. Only in poor countries, such as Zimbabwe, with their primitive financial sectors, does inflation remain lucrative for governments.

For more on hyperinflations, bank reserves, and central banks, see Hyperinflation, Money Supply, and Federal Reserve System in the Concise Encyclopedia of Economics.

The current financial crisis, moreover, has reinforced the trend toward lower seigniorage. Buried within the October 3, 2008 bailout bill, which set up the Troubled Asset Relief Program (TARP), was a provision permitting the Fed to pay interest on bank reserves, something other major central banks were doing already. Within days, the Fed implemented this new power, essentially converting bank reserves into more government debt. Fiat money traditionally pays no interest and, therefore, allows the government to purchase real resources without incurring any future tax liability. Federal Reserve notes will, of course, continue to earn no interest. But now, any seigniorage that government gains from creating bank reserves will completely vanish or be greatly reduced, depending entirely on the differential between market interest rates on the remaining government debt and the interest rate on reserves. The lower is this differential, the less will be the seigniorage. Indeed, this new constraint on seigniorage becomes tighter as people replace the use of currency with bank debit cards and other forms of electronic fund transfers. In light of all these factors, even inflation well into the double digits can do little to alleviate the U.S. government’s potential bankruptcy.

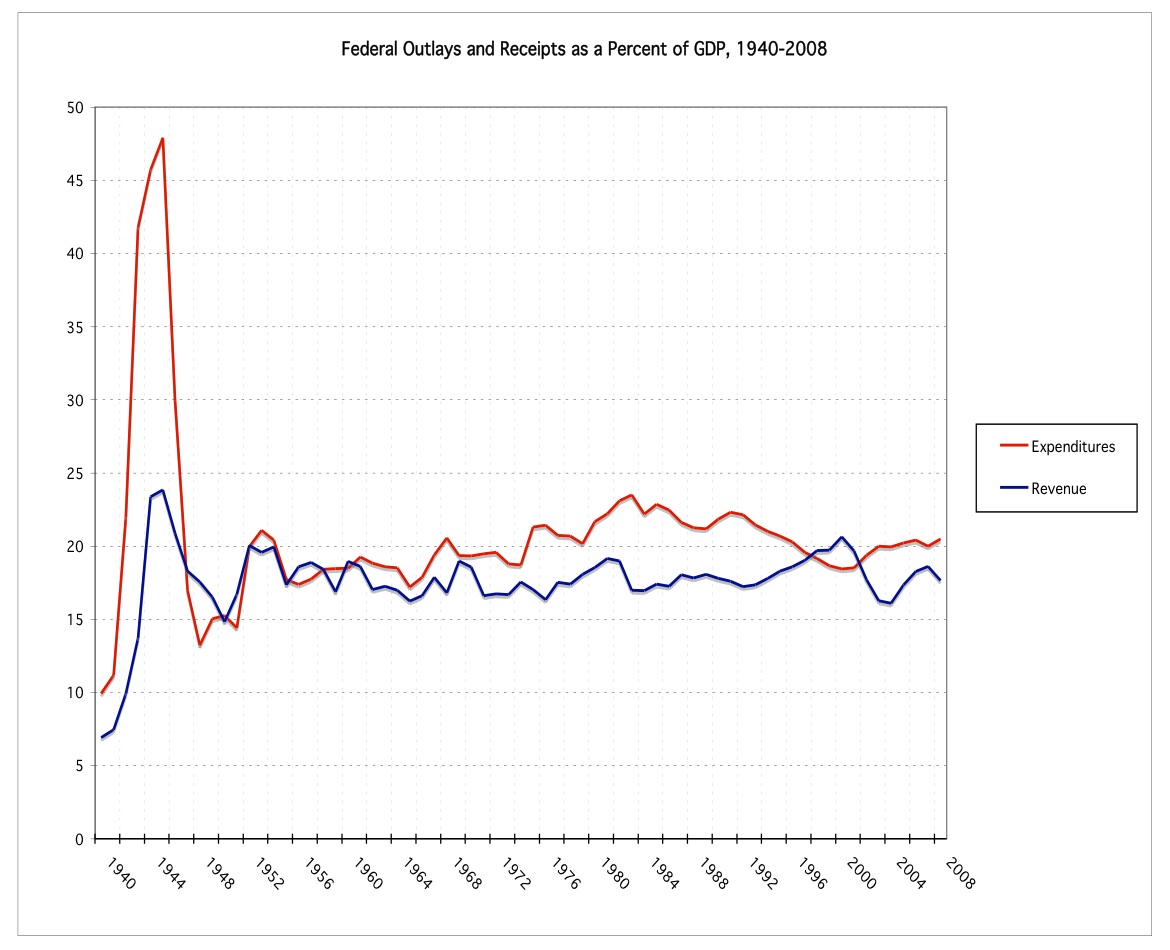

What about increasing the proceeds from explicit taxes? Examine Graph 1, which depicts both federal outlays and receipts as a percent of GDP from 1940 to 2008. Two things stand out. First is the striking behavior of federal tax revenue since the Korean War. Displaying less volatility than expenditures, it has bumped up against 20 percent of GDP for well over half a century. That is quite an astonishing statistic when you think about all the changes in the tax code over the intervening years. Tax rates go up, tax rates go down, and the total bite out of the economy remains relatively constant. This suggests that 20 percent is some kind of structural-political limit for federal taxes in the United States. It also means that variations in the deficit resulted mainly from changes in spending rather than from changes in taxes. The second fact that stands out in the graph is that federal tax revenue at the height of World War II never quite reached 24 percent of GDP. That represents the all-time high in U.S. history, should even the 20-percent-of-GDP post-war barrier prove breachable.2

Graph 1. Federal Outlays and Receipts as a Percent of GDP, 1940-2008

Compare these percentages with that of President Barack Obama’s first budget, which is slated to come in at above 28 percent of GDP. Although this spending surge is supposed to be significantly reversed when the recession is over, the administration’s own estimates have federal outlays never falling below 22 percent of GDP. And that is before the Social Security and Medicare increases really kick in. In its latest long-term budget scenarios, the Congressional Budget Office (CBO), not known for undue pessimism, projects that total federal spending will rise over the next 75 years to as much as 35 percent of GDP, not counting any interest on the accumulating debt, which critically varies with how fast tax revenues rise. However, the CBO’s highest projection for tax revenue over the same span reaches a mere 26 percent of GDP. Notice how even that “optimistic” projection assumes that Americans will put up with, on a regular peacetime basis, a higher level of federal taxation than they briefly endured during the widely perceived national emergency of the Second World War. Moreover, once you add in the interest on the growing debt because of the persistent deficits, federal expenditures in 2083, according to the CBO, could range anywhere between 44 and 75 percent of GDP.3

We all know that there is a limit to how much debt an individual or institution can pile on if future income is rigidly fixed. We have seen why federal tax revenues are probably capped between 20 and 25 percent of GDP; reliance on seigniorage is no longer a viable option; and public-choice dynamics tell us that politicians have almost no incentive to rein in Social Security, Medicare, and Medicaid. The prospects are, therefore, sobering. Although many governments around the world have experienced sovereign defaults, U.S. Treasury securities have long been considered risk-free. That may be changing already. Prominent economists have starting considering a possible Treasury default, while the business-news media and investment rating agencies have begun openly discussing a potential risk premium on the interest rate that the U.S. government pays. The CBO estimates that the total U.S. national debt will approach 100 percent of GDP within ten years, and when Japan’s national debt exceeded that level, the ratings of its government securities were downgraded.

The much (unfairly) maligned credit default swaps (CDS) in February 2009 were charging more for insurance against a default on U.S. Treasuries than for insurance against default of such major U.S. corporations as Pepsico, IBM, and McDonald’s. Because the premiums and payoffs of the CDS on U.S. Treasury securities are denominated in Euros, the annual premiums also reflect exchange-rate risk, which is probably why, with the subsequent modest decline in the dollar, CDS premiums for ten-year Treasuries fell from 100 basis points to almost 30.4 But you can make a plausible case that CDS underestimate the probability of a Treasury default since such a default could easily have far reaching financial repercussions, even hurting the counterparties providing the insurance and impinging on their ability to make good on their CDS. Surely the purchasers of the U.S. Treasury CDS have not overlooked this risk, which would be reflected in a lower annual premium for less-valuable insurance.

Predicting an ultimate Treasury default is somewhat empty unless I can also say something about its timing. The financial structure of the U.S. government currently has two nominal firewalls. The first, between Treasury debt and unfunded liabilities, is provided by the trust funds of Social Security, Medicare, and other, smaller federal insurance programs. These give investors the illusion that the shaky fiscal status of social insurance has no direct effect on the government’s formal debt. But according to the latest intermediate projections of the trustees, the Hospital Insurance (HI-Medicare Part A) trust fund will be out of money in 2017, whereas the Social Security (OASDI) trust funds will be empty by 2037.5 Although other parts of Medicare are already funded from general revenues, when HI and OASDI need to dip into general revenues, the first firewall is gone. If investors respond by requiring a risk premium on Treasuries, the unwinding could move very fast, much like the sudden collapse of the Soviet Union. Politicians will be unable to react. Obviously, this scenario is pure speculation, but I believe it offers some insight into the potential time frame.

The second financial firewall is between U.S. currency and government debt. It is not literally impossible that the Federal Reserve could unleash the Zimbabwe option and repudiate the national debt indirectly through hyperinflation, rather than have the Treasury repudiate it directly. But my guess is that, faced with the alternatives of seeing both the dollar and the debt become worthless or defaulting on the debt while saving the dollar, the U.S. government will choose the latter. Treasury securities are second-order claims to central-bank-issued dollars. Although both may be ultimately backed by the power of taxation, that in no way prevents government from discriminating between the priority of the claims. After the American Revolution, the United States repudiated its paper money and yet successfully honored its debt (in gold). It is true that fiat money, as opposed to a gold standard, makes it harder to separate the fate of a government’s money from that of its debt. But Russia in 1998 is just one recent example of a government choosing partial debt repudiation over a complete collapse of its fiat currency.

Admittedly, seigniorage is not the only way governments have benefited from inflation. Inflation also erodes the real value of government debt, and if the inflation is not fully anticipated, the interest the government pays will not fully compensate for the erosion. This happened during the Great Inflation of the 1970s, when investors in long-term Treasury securities earned negative real rates of return, generating for the government maybe one percent of GDP, or about twice as much implicit revenue as came from seigniorage. But today’s investors are far savvier and less likely to get caught off guard by anything less than hyperinflation. To be clear, I am not denying that a Treasury default might be accompanied by some inflation. Inflationary expectations, along with the fact that part of the monetary base is now de facto government debt, can link the fates of government debt and government money. This is all the more reason for the United States to try to break the link and maintain the second financial firewall. We still may end up with the worst of both worlds: outright Treasury default coupled with serious inflation. I am simply denying that such inflation will forestall default.

Still unconvinced that the Treasury will default? The Zimbabwe option illustrates that other potential outcomes, however unlikely, are equally unprecedented and dramatic. We cannot utterly rule out, for instance, the possibility that the U.S. Congress might repudiate a major portion of promised benefits rather than its debt. If it simply abolished Medicare outright, the unfunded liability of Social Security would become tractable. Indeed, one of the current arguments for the adoption of nationalized health care is that it can reduce Medicare costs. But this argument is based on looking at other welfare States such as Great Britain, where government-provided health care was rationed from the outset rather than subsidized with Medicare. Rationing can indeed drive down health-care costs, but after more than forty years of subsidized health care in the United States, how likely is it that the public will put up with severe rationing or that the politicians will attempt to impose it? And don’t kid yourself; the rationing will have to be quite severe to stave off a future fiscal crisis.

Other welfare States have higher taxes as a proportion of GDP, with Sweden and Denmark in the lead at nearly 50 percent.6 Can I really be confident that the United States will never follow their example? Let us ignore all the cultural, political, and economic differences between small, ethnically-unified European States and the United States. We still must factor in the take of state and local governments, which, together with the federal government, raises the current tax bite in the United States to 28 percent of GDP, only five percentage points below that of Canada. Recall that the CBO projects that federal spending alone for 2082 will reach almost 35 percent of GDP, excluding rising interest on the national debt. Thus, if taxes were to rise pari passu with spending, the United States might be able to forestall bankruptcy with a total tax burden, counting federal, state, and local, of around 45 percent of GDP—15 percentage points higher than the combined total at its World War II peak, higher than in the United Kingdom and Germany today, and nearly dead even with Norway and France. However, if there is any significant lag between expenditure and tax increases, the increased debt would cause the proportion to rise even more. Furthermore, this estimate relies on the CBO’s economic and demographic assumptions about the future, along with the assumption of absolutely no increase in state and local taxation as a percent of GDP. More-pessimistic assumptions also drive the percentage up.

Even conceding that federal taxes might rise rapidly enough to a level noticeably higher than during World War II overlooks an important consideration: All the social democracies are facing similar fiscal dilemmas at almost the same time. Pay-as-you go social insurance is just not sustainable over the long run, despite the higher tax rates in other welfare States. Even though the United States initiated social insurance later than most of these other welfare States, it has caught up with them because of the Medicare subsidy. In other words, the social-democratic welfare State will come to end, just as the socialist State came to an end. Socialism was doomed by the calculation problem identified by Ludwig Mises and Friedrich Hayek. Mises also argued that the mixed economy was unstable and that the dynamics of intervention would inevitably drive it towards socialism or laissez faire. But in this case, he was mistaken; a century of experience has taught us that the client-oriented, power-broker State is the gravity well toward which public choice drives both command and market economies. What will ultimately kill the welfare State is that its centerpiece, government-provided social insurance, is simultaneously above reproach and beyond salvation. Fully-funded systems could have survived, but politicians had little incentive to enact them, and much less incentive to impose the huge costs of converting from pay-as-you-go. Whether this inevitable collapse of social democracies will ultimately be a good or bad thing depends on what replaces them.

Gary M. Walton and Hugh Rockoff, History of the American Economy, 10th ed. (Mason, OH: South-Western, 2005), p. 500; Robert Higgs, “The World Wars,” in Price Fishback, et. al., History of the American Government and Economy: Essays in Honor of Robert Higgs (Chicago: University of Chicago Press, 2007); Jeffrey Rogers Hummel, “Death and Taxes, Including Inflation: The Public versus Economists,” Econ Journal Watch, 4 (January 2007): 46-59.

Data on government expenditures and revenues come from Susan B. Carter, et. al., eds., Historical Statistics of the United States: Earliest Times to the Present, Millennial ed. (New York: Cambridge University Press, 2006), v. 5, Series Ea584-678, as brought forward by Budget of the United States Government: Historical Tables Fiscal Year 2010 (Washington: U.S. Government Printing Office, 2009). Annual estimates for GDP are from Louis D. Johnston and Samuel H. Williamson, “What Was the U.S. GDP Then?” MeasuringWorth, 2008. Their GDP numbers coincide with those of the U.S. Bureau of Economic Analysis.

Office of Management and Budget, A New Era of Responsbility: Renewing America’s Promise (Washington: U.S. Government Printing Office, February 2009), Table S-1, p. 114; Doug Elmendorf, Federal Budget Challenges (Washington: Congressional Budget Office, April 2009), pp. 3-11.

A basis point is one hundredth of a percentage point.

Social Security and Medicare Boards of Trustees, Status of the Social Security and Medicare Programs: A Summary of the 2009 Annual Reports.

Organisation for Economic Co-operation and Development, Revenue Statistics 1965-2007, 2008 Edition, Table A (Paris: OECD, October 15, 2008). PDF file.