This last Wednesday I was scheduled to attend a talk in San Jose by Bryan Cutsinger, a very sharp young monetary economist from Angelo State University in Texas. But on Monday, the organizer learned that Bryan was sick and couldn’t make it. He contacted Jeff Hummel and me and asked if we could fill in. We said yes and Jeff and I organized a talk over the phone on Tuesday, with me leading in on the basics of inflation and then asking Jeff a series of questions that dug deeper and deeper into Federal Reserve monetary policy. I called it “The Hummel/Henderson Road Show on Inflation.” Jeff called it “The Ever Expanding Role of the Fed and What It Portends for the Future.” It went well.

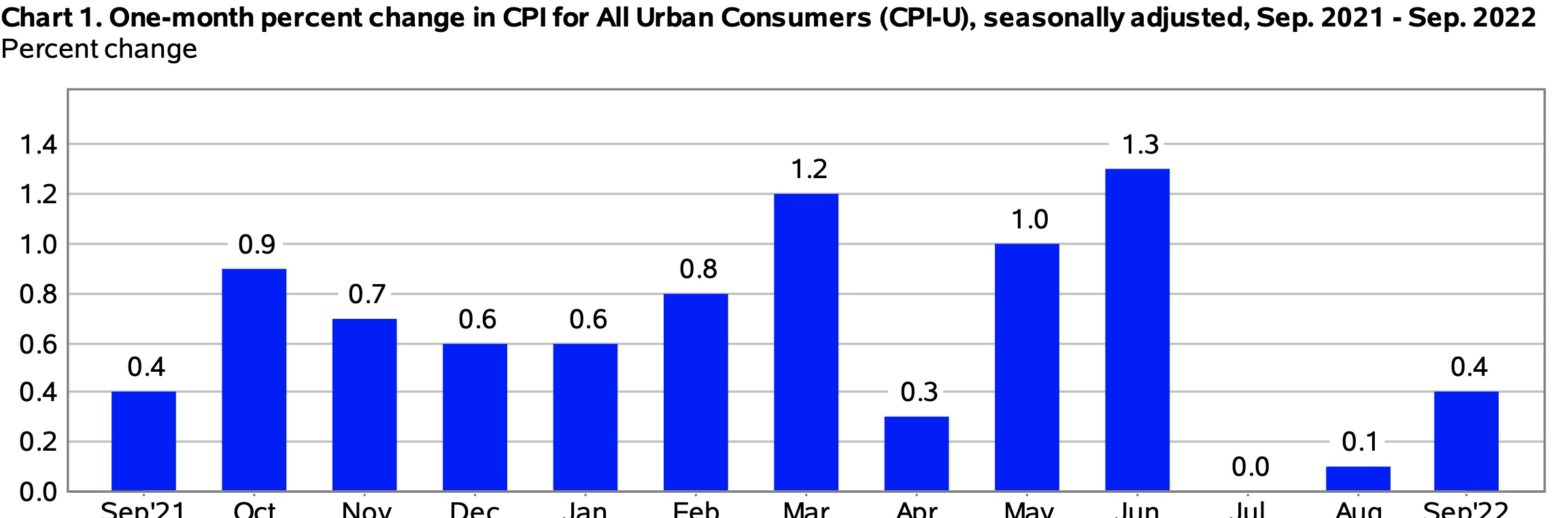

One of the items I read to prepare was an excellent piece in Forbes by Norbert Michel of the Cato Institute. He pointed out that inflation month by month has fallen. So I went to the Bureau of Labor Statistics and, sure enough, found the graph above. I presented it and said words to the effect, “Although I can’t predict inflation, I won’t be surprised if when the data come out tomorrow [that’s Thursday, November 10], they will show a monthly increase in the CPI that’s about 0.4 percent or less.”

Guess what. The data came out yesterday, Thursday, and the increase was 0.4 percent. That means that the CPI (not seasonally adjusted) rose from 296.311 in June to 298.012 in October. That’s an increase of 0.574 percent. On an annual basis, the inflation rate is 3 times that, which is 1.72 percent. So the Fed has achieved its inflation target. The seasonally adjusted CPI rose over those 4 months at an annualized rate of 2.80 percent, which means that the Fed has almost achieved its goal.

READER COMMENTS

Garrett

Nov 11 2022 at 8:47am

Shoulda bought calls!

Spencer

Nov 11 2022 at 10:35am

Contrary to Nobel Laureates Dr. Milton Friedman and Dr. Anna Schwartz’s “A Program for Monetary Stability”: the distributed lag effects of monetary flows (using the truistic monetary base, required reserves), have been mathematical constants for > 100 years.

Dr. Richard G. Anderson says: “reserves were driven by payments”.

Using a different metric,

DDs in American Yale Professor Irving Fisher’s truistic “equation of exchange”, where M*Vt = P*T

07/1/2022 ,,,,, 1.195

08/1/2022 ,,,,, 1.280 peak

09/1/2022 ,,,,, 1.143

10/1/2022 ,,,,, 1.141

11/1/2022 ,,,,, 0.906

12/1/2022 ,,,,, 0.594

01/1/2023 ,,,,, 0.603

02/1/2023 ,,,,, 0.543

03/1/2023 ,,,,, 0.459

Spencer

Nov 11 2022 at 10:36am

It’s not monetarism, which hasn’t been tried, it’s the FED’s faulty metric of inflation that’s wrong.

Jim

Nov 11 2022 at 10:56am

Core is still over 5% during that same time:

https://fred.stlouisfed.org/graph/?g=Wk6U

Fuel price increases were bad for perceptions (and headline CPI) on the way up, on the way down they have been good, but that is really besides the point. The Fed didn’t control the run up in those particular prices, and its unclear to me at least how much of the drop off in energy prices were based on decreases in demand that you can attribute to Fed policy slowing the economy as of yet.

Consumer Price Index Summary – 2022 M10 Results (bls.gov)

Jim

Nov 11 2022 at 10:58am

Here is the last link:

https://www.bls.gov/news.release/cpi.nr0.htm

Scott Sumner

Nov 11 2022 at 11:57am

Two points:

1. I think you mean annual inflation is 4 times the 3 month rate.

2. The Fed has an average inflation target of 4%, where the average is not specified but generally assumed to be over a period of a few years. So on that basis the Fed has not achieved its target, although the past three months are certainly an improvement.

Unfortunately, many people believe the next three months will be worse, as the “headline” CPI was recently affected by the sharp fall in gasoline prices. The core CPI is often a better indicator of the underlying trend going forward.

robc

Nov 11 2022 at 1:26pm

RE: #1

I was going to post the same thing, but he posted June to October, which is 4 months, so multiplying by 3 is correct(ish). 1.00574^3 is 1.73%, not 1.72%, but close enough as I don’t believe inflation can ever remotely be measured accurately to 3 decimal places. Not completely sure about 1.

David Henderson

Nov 11 2022 at 3:43pm

On #1, no I don’t. See robc’s response. It’s 4 months of inflation data, not 3.

Thomas Lee Hutcheson

Nov 12 2022 at 12:17pm

Isn’t the Fed’s average inflation target 2% PCE = ~2.3% CPI?

Thomas Lee Hutcheson

Nov 13 2022 at 7:18am

I also suggest keeping an eye on the TIPS. There bond traders seem to be expecting inflation over 5 and 10 year periods to be near, but still above the Fed’s target. What a shame that the Treasury doe not provide us with more intermediate tenor TIPS — 6 mo., 1, 2, 3 year tenors!

dennis e miller

Dec 1 2022 at 3:31pm

So I’ve had this article stewing on the back burner of my brain for a couple weeks and finally can no longer stop myself from commenting. At this long of a delay, I hope someone reads my comment.

So this article is a joke, right? You do some calculations and near the end make the statement “The seasonally adjusted CPI rose over those 4 months at an annualized rate of 2.80 percent, which means that the Fed has almost achieved its goal.” Hahahaha. You aren’t serious, right? Playing fast and fancy with time frames gives different results. Suppose I was an insomniac that needs 7 hours of sleep but only get 4 hours per day. However if I measure my sleeping hours only between 10pm and 6am I would find that I slept 4 out of 8 hours. Then I could convert that to a daily sleeping rate of 12 hours per day and decide I’m not an insomniac at all — I’m actually getting plenty of sleep according to this calculation method. That’s what your article does. It mingles inflation numbers for M2M and Y2Y. I think we all understand that when the Federal reserve says around 2% inflation that they imply Y2Y. So you can’t take a 4-month sample period, calculate an annual rate from that, treat it as Y2Y and say that the goal is met, or nearly met. It needs to be met for a year to have Y2Y inflation at 2%, not just 2, 3 or 4 months.

I remember at one point in the past year that Biden said inflation was “zero”. I immediately thought of an analogy. Biden is on a cargo airplane and accidentally falls out the cargo door without a parachute. Gravity starts to accelerate him downwards and with every passing he notices that gravity is making him fall at a faster speed than a second ago. Biden thinks to himself “If only I could make my speed “zero”…”. After a while his speed is fast enough that air resistance starts to become a significant factor. Eventually the force of the air resistance equals the downward force due to gravity and Biden reaches what is known as “terminal velocity.” He thinks to himself “Hooray, I measured my speed 10 seconds ago, 5 seconds ago and just now and there is no change. Therefore my speed is ‘zero’ and all is well.”

There is a huge difference between an average value over a timeframe (such as Y2Y) and an instantaneous value (or average value over a much shorter timeframe such as M2M).

Comments are closed.