One can think of the past 100 years of US history as featuring three macro regimes:

1. Commodity money, with alternating periods of rising and falling prices.

2. Unanchored fiat money, with rising and falling inflation rates.

3. 2% inflation targeting.

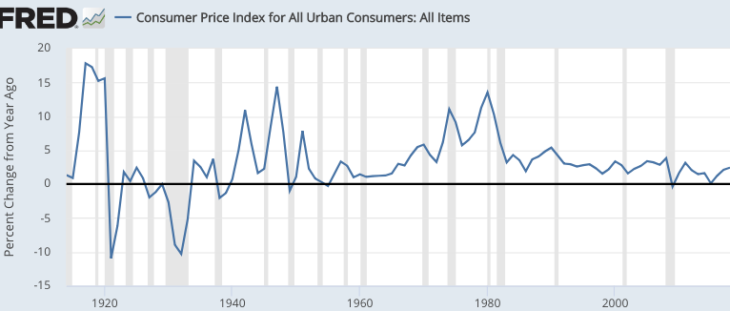

Both transitions occurred gradually, so it’s not possible to assign precise dates, but 1940 and the early 1990s are plausible estimates. Here is the CPI inflation rate since 1913:

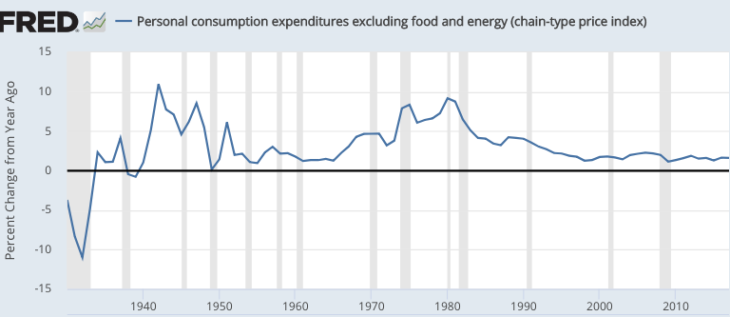

The Fed has a flexible inflation target, where it does not try to achieve precisely 2% inflation each year. In addition, they target the PCE price index, not the CPI. Thus if oil prices rise sharply, they generally allow the CPI to rise modestly above 2%, for a time. Here’s the core PCE inflation rate, but only since 1930:

The Fed has a flexible inflation target, where it does not try to achieve precisely 2% inflation each year. In addition, they target the PCE price index, not the CPI. Thus if oil prices rise sharply, they generally allow the CPI to rise modestly above 2%, for a time. Here’s the core PCE inflation rate, but only since 1930:

Over the last 25 years, core PCE inflation has fluctuated in a tight range, from a high of 2.28% at the peak of the housing boom (2006) to a low of 1.16% in the depths of the Great Recession (2009.) Even that overstates the actual variation in non-food/energy prices, as core inflation is still somewhat affected by oil prices (think airfares, freight charges, etc.)

Many people focus on how the Fed often misses its 2% target, or treats it as a ceiling, and those are important issues. But doing so risks overlooking more important trends. Thus if the Fed were to treat 2% as an inflation ceiling, one might think of them as actually targeting inflation at something like 1.6% or 1.8%. I’m not sure that’s true, but even a 1.6% inflation target would have important implications.

The transition away from commodity money that begins to show up in the data after 1940 was essentially complete by 1968, at which time macroeconomics had to be reinvented. With fluctuating inflation expectations, we needed new ideas such as the Natural Rate Hypothesis and the Taylor Principle, which were not required under a commodity money regime with roughly zero percent expected inflation.

The current regime of 2% inflation targeting calls for another reinvention of macro. I’m not sure people have fully grasped how much everything changes under inflation targeting. Consider this recent comment by Tyler Cowen:

Finally, if the carbon tax is revenue-neutral, just sending money to everyone (in what proportions?) doesn’t give them anything in return as measured by real resources. Maybe it would give Jay Powell a slight headache, however, since he and others at the Fed would have to decide whether and how to do an offset, or not.

I agree with Tyler that it’s unwise to rebate carbon tax revenue to the public (I’d use it for deficit reduction.) I also agree that the Fed might need to consider how to offset this policy. (Although a combination of tax and rebate would probably not have much impact on demand, requiring only a small offset.) Where I disagree is the claim that “the Fed would have to decide whether” to offset. Perhaps it’s a throwaway line, but I see it as the type of thinking that is now outdated.

Suppose a big rebate program is announced, and suppose it would materially boost AD if not offset. How will the Fed react? There is almost no chance that the next FOMC meeting would feature Fed officials saying “because of the rebate, we should shift our target from 2% inflation to 2.2% inflation”. Is there a chance that they would nonetheless do exactly that, but keep it secret? I suppose anything is possible, but I don’t see any evidence that they’d even wish to do this. That’s certainly not how they act; they are frequently nudging rates up and down to try to keep inflation close to 2%.

So if I am right, why is this not better accepted? I believe that many people put too much weight on the fact that inflation targeting isn’t perfect, and that the Fed rarely achieves exactly 2% inflation. Maybe they are even slightly biased toward “lowflation”. But that fact has little bearing on the question of whether the Fed would try to offset any particular demand shock, rather it suggests their current tool kit is far from perfect. The Fed has moved well beyond the “whether” question; now it’s all about the “how” question.

In this new world of inflation targeting it is still possible that a fiscal shock (or some other sort of demand shock) will impact aggregate spending. Fed offset is far from perfect. Rather, what’s new about the post-1990 world is that fiscal shocks are no longer expected to have any specific impact. It’s equally likely that the Fed will do too much to offset, as too little. The new baseline assumption is no effect on average, not in every single case.

This new 2% inflation world has also proved challenging for me. My toolkit is mostly monetarist, ideally suit for the high and volatile inflation rates seen all over the world between 1950-1990. Ideas like the Fisher effect and the Natural Rate Hypothesis are (or were) my primary tools for thinking about macro issues. And now we live in a world where the Fisher effect has virtually gone away, and the Natural Rate Hypothesis seems almost useless. Inflation expectations are stuck at roughly 2%. It’s increasingly hard for me to find useful things to say our 21st century economy.

But that’s not because the world has changed in any “structural” sense, rather that the policy regime has changed. When I was young, idealistic reformers thought the Phillips Curve was structural, and could be exploited to create millions of jobs for unemployed workers. Later we discovered that this would not work. Robert Lucas showed that structural parameters that look stable (like the Phillips Curve) are not reliable when the policy regime changes.

Recently I see more and more idealistic young people (who don’t recall the Great Inflation) recommending policy initiatives that are based on the notion that “inflation is dead”, not worth worrying about anymore. Yes, inflation is currently dead (or at least low and stable), but that’s only because we are not trying to take advantage of low inflation expectations by using monetary and fiscal policy to finance “populist” policies. It is not because demographics, or global competition, or technological change are creating a structurally low inflation rate.

PS. For the purposes of this post, I assume that fiscal shocks have little impact on aggregate supply. In most cases, I believe that’s a reasonable assumption. The recent corporate tax cut, however, probably slightly boosted AS.

READER COMMENTS

Benjamin Cole

Jan 19 2019 at 7:44pm

Interesting post. I disagree perhaps in that I think macroeconomic policymakers should try to take advantage of low-inflation expectations to increase output and employment.

Beyond that, does a successful monetary policy rely to a large degree on “behavioral economics”? A successful monetary policy relies upon the soft squishy mushy concept of “people’s expectations“?

I wonder if there is not something else afoot, as inflation rates have fallen globally, even in those nations such as Japan that engage in extensive QE and constantly signal that they are attempting to reach a higher rate of inflation. Of course there is a tautological answer: people in Japan expected Bank of Japan to fail in its mission.

All of this suggests that sociology and the shaping of public opinion is a major part of modern macroeconomics.

Benjamin Cole

Jan 19 2019 at 8:01pm

Another troubling observation: is obtaining a 2% inflation target only possible through chronic monetary suffocation?

Are there consequences of a 2% inflation target, such as wage stagnation?

Wages have been almost perfectly stagnant since year 2000 and the era of price stability.

Benjamin Cole

Jan 19 2019 at 9:59pm

Add on (apologies, but this may be important):

The Reserve Bank of Australia has had decades of success with an inflation band target of 2% to 3%. They formalized the inflation target band in the early 1990s, and famously have not had a recession since,

The RBA has even tolerated or incurred inflation bouts of 4%, but was either able or lucky enough to bring inflation back down into the 2% to 3% inflation band target, without incurring a recession. The RBA has been under-shootiing its band since 2014, despite exploding house prices.

This RBA track record seems to slay the “Runaway Inflation Goblin-Totem” so prominently placed in the Temple of Macroeconomics. A central bank can tolerate 4% inflation for a while, and not inevitably incur runaway inflation—-that is the historical track record in Australia, not a theory.

Of course, if we believe popular expectations matter, we can conclude that RBA can tolerate 4% inflation from time to time, as the public expects them to bring inflation back down into the inflation band eventually. The RBA has street cred.

But, egads! I say to pointy-headed, frizzy-haired sociologists Phd’s of the world, this is your hour!

Modern macroeconomics and monetary policy rests upon a galaxy-sized jello pad-foundation of popular anticipation, mood and expectations.

And why is inflation in Australia now below target? I don’t know. The tautological answer is the public expects the RBA to miss its target. But why?

The key RBA rate is now 1.5%.

Add an “h” to the front of links, to activate.

https://fred.stlouisfed.org/series/FPCPITOTLZGAUS

https://fred.stlouisfed.org/series/NAEXKP01AUQ657S

BC

Jan 20 2019 at 7:34am

“…’inflation is dead’, not worth worrying about anymore.”

That’s also why we don’t need speed limits on expressways anymore. Hardly anyone (significantly) speeds anyways. Maybe, there are demographic or technological reasons why everyone seems to drive at about 5-10 mph above the limit. It also may have been pure coincidence that, when non-urban speed limits rose from 55 to 65-70, driving speeds seemed to have risen by about 10-15 mph.

Kurt Schuler

Jan 20 2019 at 9:51am

By the Natural Rate Hypothesis, are you referring to Milton Friedman’s natural rate of employment, or to Knut Wicksell’s natural rate of interest? The former indeed seems not so relevant to the U.S. at present because the labor force participation rate, especially among prime age men, still has room to increase substantially. The latter explains why the Fed has been raising its target interest rate rather than standing pat.

Scott Sumner

Jan 20 2019 at 12:35pm

BC, Good analogy.

Kurt, I am referring to Friedman’s natural rate theory. It explained how the Phillips curve shifted when expected inflation changed. But now expected inflation is stable, so the Philips curve no longer seems to shift.

I still think his theory is true, but it’s no longer as useful as during earlier decades.

I agree that the LFPR for prime age men has room to expand substantially, but I don’t believe it will do so. It’s been declining since the 1950s, and I see nothing that would change that pattern.

Robert Schadler

Jan 20 2019 at 1:52pm

Would be interested in seeing some discussion about the merit of any part of the government trying to induce any rate of inflation.

Is there not some merit in seeing inflation by government policy as an undemocratic (“we the people” had no say in its enactment as policy) and regressive (the poor are more affected by a x% decrease in their nominal money income and holdings) than are the wealthy.

Yes, the wealthy and well paid may lose more in dollar amounts, but their marginal utility for that money is likely less — and they have a much easier path to shield themselves from the negative effects of inflation.

While I might favor a flat tax, in a democratic republic those who do should persuade enough other people to make it a policy. And while government induced inflation, of any rate, might not be deemed “theft” (Rueff?) it is at least a reduction in the worth of nominal money.

robc

Jan 21 2019 at 10:07am

My thought is, “why not target 0% instead of 2%”.

That is the natural inflation rate in Regime #1 with commodity money.

I would think a regime #3 targeting 0% would get the natural inflation rate of regime #1 without the large short term swings of inflation/deflation.

I have a preference for commodity money over fiat money, but if we are going to have fiat money and a FED, might as well target the commodity money natural inflation rate.

Scott Sumner

Jan 21 2019 at 12:44pm

Robert, I don’t favor having the Fed target inflation. The official inflation numbers are not very meaningful; it’s not clear what they are trying to describe.

robc

Jan 21 2019 at 2:47pm

Good point. I will just stick with my initial preference of going back to regime #1 and not targeting anything.

Brian Donohue

Jan 21 2019 at 1:08pm

Yes, the current 2% inflation regime has been very successful.

Except for that one time.

LK Beland

Jan 23 2019 at 4:14pm

Interesting post.

One comment about:

In the medium-to-long run, if carbon reduction policies are successful, we’d expect carbon-tax revenue to be quite small. If we finance deficit-reduction with the carbon-tax, we will eventually have to find another source of revenue to replace it. In the medium-to-long run, we have to find another way to reduce the deficit. Implementing these solutions now seems more sustainable than temporarily relying on a carbon tax.

I think that it is wiser to rebate the carbon tax to the public, and phase-out the rebate as the carbon tax revenue decreases.

Comments are closed.