Fiscal Policy

By David N. Weil

Fiscal policy is the use of government spending and taxation to influence the economy. When the government decides on the goods and services it purchases, the transfer payments it distributes, or the taxes it collects, it is engaging in fiscal policy. The primary economic impact of any change in the government budget is felt by particular groups—a tax cut for families with children, for example, raises their disposable income. Discussions of fiscal policy, however, generally focus on the effect of changes in the government budget on the overall economy. Although changes in taxes or spending that are “revenue neutral” may be construed as fiscal policy—and may affect the aggregate level of output by changing the incentives that firms or individuals face—the term “fiscal policy” is usually used to describe the effect on the aggregate economy of the overall levels of spending and taxation, and more particularly, the gap between them.

Fiscal policy is said to be tight or contractionary when revenue is higher than spending (i.e., the government budget is in surplus) and loose or expansionary when spending is higher than revenue (i.e., the budget is in deficit). Often, the focus is not on the level of the deficit, but on the change in the deficit. Thus, a reduction of the deficit from $200 billion to $100 billion is said to be contractionary fiscal policy, even though the budget is still in deficit.

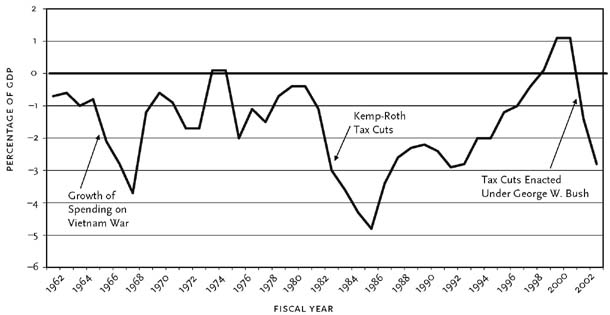

Figure 1 shows the federal budget surplus over the period 1962–2003. The data in the figure are corrected to remove the effects of business cycle conditions. For example, in fiscal year 2003, the actual budget deficit was $375 billion, of which an estimated $68 billion was due to the lingering effects of a recession, so that the cyclically adjusted deficit was $307 billion. The data are also “standardized” to eliminate the effects of inflation and the effects of quirks in the timing of revenues and outlays, such as the receipt of payments from Desert Storm allies that arrived in the fiscal years following the war itself. Notable on the figure are the fiscal stimulus of the Vietnam War, the Kemp-Roth tax cuts of the early 1980s, and the program of tax cuts enacted under George W. Bush.

The most immediate effect of fiscal policy is to change the aggregate demand for goods and services. A fiscal expansion, for example, raises aggregate demand through one of two channels. First, if the government increases its purchases but keeps taxes constant, it increases demand directly. Second, if the government cuts taxes or increases transfer payments, households’ disposable income rises, and they will spend more on consumption. This rise in consumption will in turn raise aggregate demand.

Fiscal policy also changes the composition of aggregate demand. When the government runs a deficit, it meets some of its expenses by issuing bonds. In doing so, it competes with private borrowers for money loaned by savers. Holding other things constant, a fiscal expansion will raise interest rates and “crowd out” some private investment, thus reducing the fraction of output composed of private investment.

In an open economy, fiscal policy also affects the exchange rate and the trade balance. In the case of a fiscal expansion, the rise in interest rates due to government borrowing attracts foreign capital. In their attempt to get more dollars to invest, foreigners bid up the price of the dollar, causing an exchange-rate appreciation in the short run. This appreciation makes imported goods cheaper in the United States and exports more expensive abroad, leading to a decline of the merchandise trade balance. Foreigners sell more to the United States than they buy from it and, in return, acquire ownership of U.S. assets (including government debt). In the long run, however, the accumulation of external debt that results from persistent government deficits can lead foreigners to distrust U.S. assets and can cause a deprecation of the exchange rate.

Source: Congressional Budget Office, Washington, D.C.

Fiscal policy is an important tool for managing the economy because of its ability to affect the total amount of output produced—that is, gross domestic product. The first impact of a fiscal expansion is to raise the demand for goods and services. This greater demand leads to increases in both output and prices. The degree to which higher demand increases output and prices depends, in turn, on the state of the business cycle. If the economy is in recession, with unused productive capacity and unemployed workers, then increases in demand will lead mostly to more output without changing the price level. If the economy is at full employment, by contrast, a fiscal expansion will have more effect on prices and less impact on total output.

This ability of fiscal policy to affect output by affecting aggregate demand makes it a potential tool for economic stabilization. In a recession, the government can run an expansionary fiscal policy, thus helping to restore output to its normal level and to put unemployed workers back to work. During a boom, when inflation is perceived to be a greater problem than unemployment, the government can run a budget surplus, helping to slow down the economy. Such a countercyclical policy would lead to a budget that was balanced on average.

Automatic stabilizers—programs that automatically expand fiscal policy during recessions and contract it during booms—are one form of countercyclical fiscal policy. Unemployment insurance, on which the government spends more during recessions (when the unemployment rate is high), is an example of an automatic stabilizer. Similarly, because taxes are roughly proportional to wages and profits, the amount of taxes collected is higher during a boom than during a recession. Thus, the tax code also acts as an automatic stabilizer.

But fiscal policy need not be automatic in order to play a stabilizing role in business cycles. Some economists recommend changes in fiscal policy in response to economic conditions—so-called discretionary fiscal policy—as a way to moderate business cycle swings. These suggestions are most frequently heard during recessions, when there are calls for tax cuts or new spending programs to “get the economy going again.”

Unfortunately, discretionary fiscal policy is rarely able to deliver on its promise. Fiscal policy is especially difficult to use for stabilization because of the “inside lag”—the gap between the time when the need for fiscal policy arises and when the president and Congress implement it. If economists forecast well, then the lag would not matter because they could tell Congress the appropriate fiscal policy in advance. But economists do not forecast well. Absent accurate forecasts, attempts to use discretionary fiscal policy to counteract business cycle fluctuations are as likely to do harm as good. The case for using discretionary fiscal policy to stabilize business cycles is further weakened by the fact that another tool, monetary policy, is far more agile than fiscal policy.

Whether for good or for ill, fiscal policy’s ability to affect the level of output via aggregate demand wears off over time. Higher aggregate demand due to a fiscal stimulus, for example, eventually shows up only in higher prices and does not increase output at all. That is because, over the long run, the level of output is determined not by demand but by the supply of factors of production (capital, labor, and technology). These factors of production determine a “natural rate” of output around which business cycles and macroeconomic policies can cause only temporary fluctuations. An attempt to keep output above its natural rate by means of aggregate demand policies will lead only to ever-accelerating inflation.

The fact that output returns to its natural rate in the long run is not the end of the story, however. In addition to moving output in the short run, expansionary fiscal policy can change the natural rate, and, ironically, the long-run effects of fiscal expansion tend to be the opposite of the short-run effects. Expansionary fiscal policy will lead to higher output today, but will lower the natural rate of output below what it would have been in the future. Similarly, contractionary fiscal policy, though dampening the output level in the short run, will lead to higher output in the future.

A fiscal expansion affects the output level in the long run because it affects the country’s saving rate. The country’s total saving is composed of two parts: private saving (by individuals and corporations) and government saving (which is the same as the budget surplus). A fiscal expansion entails a decrease in government saving. Lower saving means, in turn, that the country will either invest less in new plants and equipment or increase the amount that it borrows from abroad, both of which lead to unpleasant consequences in the long term. Lower investment will lead to a lower capital stock and to a reduction in a country’s ability to produce output in the future. Increased indebtedness to foreigners means that a higher fraction of a country’s output will have to be sent abroad in the future rather than being consumed at home.

Fiscal policy also changes the burden of future taxes. When the government runs an expansionary fiscal policy, it adds to its stock of debt. Because the government will have to pay interest on this debt (or repay it) in future years, expansionary fiscal policy today imposes an additional burden on future taxpayers. Just as the government can use taxes to transfer income between different classes, it can run surpluses or deficits in order to transfer income between different generations.

Some economists have argued that this effect of fiscal policy on future taxes will lead consumers to change their saving. Recognizing that a tax cut today means higher taxes in the future, the argument goes, people will simply save the value of the tax cut they receive now in order to pay those future taxes. The extreme of this argument, known as Ricardian equivalence, holds that tax cuts will have no effect on national saving because changes in private saving will exactly offset changes in government saving. If these economists were right, then my earlier statement that budget deficits crowd out private investment would be wrong. But if consumers decide to spend some of the extra disposable income they receive from a tax cut (because they are myopic about future tax payments, for example), then Ricardian equivalence will not hold; a tax cut will lower national saving and raise aggregate demand. Most economists do not believe that Ricardian equivalence characterizes consumers’ response to tax changes.

In addition to its effect on aggregate demand and saving, fiscal policy also affects the economy by changing incentives. Taxing an activity tends to discourage that activity. A high marginal tax rate on income reduces people’s incentive to earn income. By reducing the level of taxation, or even by keeping the level the same but reducing marginal tax rates and reducing allowed deductions, the government can increase output. “Supply-side” economists argue that reductions in tax rates have a large effect on the amount of labor supplied, and thus on output (see supply-side economics). Incentive effects of taxes also play a role on the demand side. Policies such as investment tax credits, for example, can greatly influence the demand for capital goods.

The greatest obstacle to proper use of fiscal policy—both for its ability to stabilize fluctuations in the short run and for its long-run effect on the natural rate of output—is that changes in fiscal policy are necessarily bundled with other changes that please or displease various constituencies. A road in Congressman X’s district is all the more likely to be built if it can be packaged as part of countercyclical fiscal policy. The same is true for a tax cut for some favored constituency. This naturally leads to an institutional enthusiasm for expansionary policies during recessions that is not matched by a taste for contractionary policies during booms. In addition, the benefits from expansionary policy are felt immediately, whereas its costs—higher future taxes and lower economic growth—are postponed until a later date. The problem of making good fiscal policy in the face of such obstacles is, in the final analysis, not economic but political.

About the Author

David N. Weil is a professor of economics at Brown University.

Further Reading

Nontechnical

Advanced

Web Link