Robert Barro recently asserted that the US entered a recession in early 2022:

The bottom line is that, with the announcement on July 28 of a two-quarter GDP decline, we can be highly confident that the US economy entered a recession early in 2022.

I believe that claim is extremely unlikely to be true, although it’s quite possible that we are about to enter a recession. Barro points out that since WWII, two consecutive quarters of negative RGDP have invariably been associated with recessions. So why is he wrong about early 2022?

There are several mistakes that people make when looking for statistical patterns. One is data mining. Thus they might notice that Super Bowl wins from former AFL teams are almost always associated with a certain stock market performance. Once the pattern is discovered, it usually proves unreliable going forward, as there is no reason to expect such a correlation. Barro is not guilty of that sin. It has long been known that falling GDP is a good rule of thumb for there being a recession, and for good reason. He is not engaged in data mining.

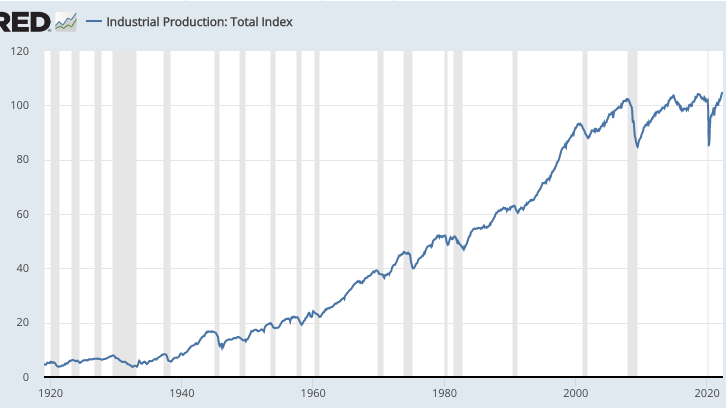

Barro is guilty of another mistake, however. He doesn’t pay enough attention to other important information that tends to conflict with his claim. For instance, it’s also a good rule of thumb that industrial production always falls during recessions. Always. No exceptions. And yet industrial production rose very rapidly during the first 6 months of 2022 (at an annual rate of 5%):

Here’s another reliable pattern. Payroll employment usually falls during recessions. In a few occasions such as 1974 and 1980, it rose modestly during the early months of recession. But even then the rate of growth was slowing. Furthermore, the 1970s and early 1980s was a period of very rapid growth in the labor force–the trend in employment was sharply higher (as both boomers and women entered the labor force in large numbers.)

In recent years, in contrast, we have very slow growth in the labor force, mostly due to sharply lower immigration and retiring boomers. And yet despite that very slow underlying growth in the labor force, employment in the first 6 months of 2022 grew at a phenomenal rate of 461,333/month. Nothing like that has ever happened before during a recession. Indeed not only is that an above normal rate of growth in employment, it is faster growth in employment than the US normally sees during an economic boom. And the second half of the year began with the economy still red hot, as 528,000 jobs were added in July.

Indeed there is a wide range of indicators whose behavior is completely inconsistent with the notion that the economy was in recession in early 2022. One of those indicators is real GDP measured using the “income method”. That’s right, the US measures real GDP in two different ways, and one of those methods actually showed positive growth in the first quarter.

Instead of focusing on one metric, the NBER relies on wide variety of monthly indicators such as payroll employment and industrial production, not just quarterly GDP. Most of those suggest that the US experienced a strong economic boom in the early months of 2022. It seems very unlikely to me that the NBER will date the recession as beginning in the first quarter. I even doubt that a recession began in the second quarter, although I’d say that’s somewhat more likely (say a 10% chance, vs. a 1% chance in Q1.)

I suspect that many economists don’t know that the quality of US macro data has been declining for many decades. Modern economies are much harder to measure than the commodity-based economies of 100 years ago. That’s why we see so many bizarre anomalies in the data for variables such as GDP.

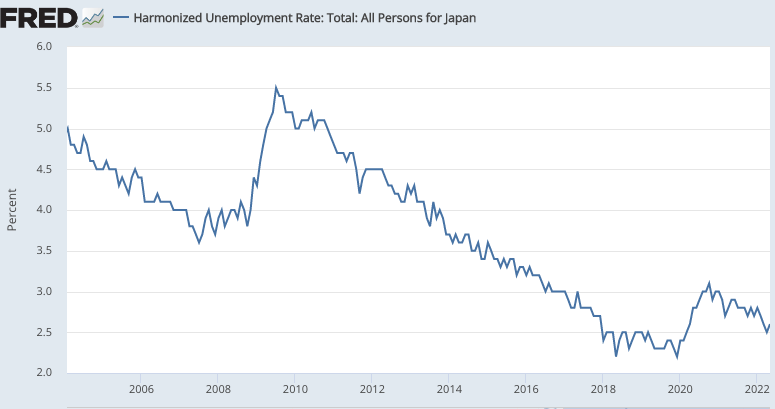

In some respects, it’s even worse in other countries. Unlike the US, many countries do use two negative quarters as an official definition of recession. This leads to some pretty absurd claims; such as that Japan has had 4 recessions since 2007! Oddly, their unemployment rate data shows only 2 of the 4 recessions:

In previous posts, I’ve called the other two recessions (during the 2010s) “phony recessions”. The problem here is that Japan’s trend rate of RGDP growth has fallen to such a low level that even a tiny slowdown can briefly push RGDP growth below zero. When there’s an actual recession (as during the global crisis of 2008 and the Covid crisis), you see a noticeable rise in the Japanese unemployment rate. In contrast, when there’s a brief slowdown, say due to the timing of purchases around a Japanese sales tax increase, the labor market is largely unaffected.

If people insist on calling those minor slowdowns “recessions”, that’s their prerogative. But if you are going to do so, don’t act like recessions matter at all.

You say that Japan had recessions in 2011 and 2014? Oh really, and why should I care?

PS. You may be wondering about the fall in US industrial production during 2016. That wasn’t a recession, but it did hurt certain sectors on the economy. It was caused by a combination of tight money and a drop in fracking (which uses a lot of equipment made in the USA.) It probably cost Hillary Clinton the election, as it hit Pennsylvania, Michigan and Wisconsin harder than other states. But in retrospect, I suspect Trump would have won in 2020 if he’d lost in 2016, so it all evens out in the long run.

PPS. Hillary would have reappointed Yellen, who would have implemented a less inflationary policy, benefiting Trump in 2021. Trump appointed Powell, who was reappointed by Biden. Powell’s inflationary policies have made things more difficult for Biden. It’s funny how things work out.

READER COMMENTS

vince

Aug 5 2022 at 3:14pm

In the Henderson blog on Definitions of Recession, Richard A pointed out that GDI was up 1.8% Q1 2022. GDI is GDP too. In July unemployment declined to 3.5%. How can anyone be sure yet that this is a recession?

Scott Sumner

Aug 5 2022 at 5:10pm

There may be a recession soon, but there certainly wasn’t a recession last winter.

vince

Aug 5 2022 at 3:32pm

It will be interesting to see how the Phillips curve unrolls. Unemployment is low and going down. At the same time, TIPS breakeven inflation five months ahead is about 3.5% and one year ahead 3%.

Matthias

Aug 6 2022 at 7:46pm

The Phillips curve hasn’t been a thing since they got off the gold standard..

BK

Aug 5 2022 at 5:40pm

Do you have a reference post for your personal definition of a recession? Something along the lines of “a decline in the average living standard of a citizen as a result of a deterioration of economic conditions” or the like? It would make it easier to understand what you’re arguing for rather than just against.

Scott Sumner

Aug 6 2022 at 1:18pm

Both Barro and I are referring to the same thing—the NBER’s definition, which takes many data series into account. (It’s a subjective call, there is no strict formula.)

Mark Brophy

Aug 9 2022 at 12:16pm

It’s like the Supreme Court definition of pornography, “I know it when I see it.”

artifex

Aug 5 2022 at 10:26pm

There has been much pushback (including some high profile) on the two-consecutive-quarters recession claims, so maybe the NBER committee will make the right call after all. I’m very uncertain about that now.

Michael Sandifer

Aug 6 2022 at 10:13am

Yes, there may be a recession soon, but I think it’s unlikely at this point, sans significant negative nominal or real shocks. I agree completely that there hasn’t been a recession this year.

Zeke5123

Aug 6 2022 at 12:52pm

I am not sure the employment numbers are trustworthy. I recall they changed methodology for adjustments at the start of the year which led to a big beat. We had a massive beat on this employment report, largely driven by adjustments. Other data sources seemingly disagree with the employment data (eg household survey).

I wonder if the numbers are just different due to the change in methodology.

Scott Sumner

Aug 6 2022 at 1:23pm

That’s possible, but many other series also conflict with the recession claim. Did the industrial production index change at the same time? There’s never been a recession with rapidly rising IP.

Also, why are so many companies unable to find workers? I’ve never seen such bad service in my entire life.

And why did real GDI rise in the first quarter? I suspect if there is a recession, it will have begun sometime after last winter.

Mark Brophy

Aug 9 2022 at 12:21pm

The government paid us to stay home during CovidMania and we enjoyed leisure so much that we haven’t returned to work. Perhaps, we never will.

bill

Aug 6 2022 at 7:38pm

Since the calculation of RGDP depends on an accurate measure of inflation, could an issue just be that the GDP deflator is miscalculated? Especially at a time when the basket of goods and services has been in flux due to covid?

Scott Sumner

Aug 7 2022 at 1:22pm

Yes, that’s possible.

Thomas Lee Hutcheson

Aug 7 2022 at 8:46am

I just cannot understand the interest in determining if we are, were, or will be in a “recession.” what decision does or ought to turn on that determination?

vince

Aug 8 2022 at 8:34pm

Here’s one: political party talking points. Party above country.

Michael Rulle

Aug 11 2022 at 7:41am

2021+2022 (EST) had average tax receipts of about 18% of GDP—-surprisingly normal. They had average expenditures of about 29% of GDP——shockingly abnormal—-lower only than WWII——which Truman took down by 2/3rds in a few years.

That was “Covid” caused—-not really —-it was our “response to Covid”caused.

That is a lot of monetary offset. Particularly since our spending forecasts are 24-25% of GDP. Taxes never hit 20% (they did hit 20.1 under Clinton when we had a surplus—and 20.o in 1944)——-so Powell will be presumably doing a lot of “offsetting”

NGDPLT will never happen——-well—-maybe not never—-but not in the next 5 years or more.

Comments are closed.